Profitability & Channel Mix in DTC Brand Valuations

DTC brand valuation discussions in 2024 often focus on factors such as the importance of profitability over revenue growth and the presence of a strong retail channel. But how much of an impact do these factors really have? With relatively few private market DTC transactions taking place over the past two years, brand owners have few comparators. This is where public market data can be very useful in helping us to understand the factors affecting the valuation of DTC & retail brands.

Background

Profitability is obviously central to valuation. Income valuation models are based on the core principle that an asset (such as a business) is worth the sum of its future cash flows. But what about those companies that are not profitable (especially those for whom profitability is in the distant future)? A different valuation approach is required.

In some sectors, signals such as revenue growth are taken as a proxy for the eventual profitability of the business – technology is the classic example, but during the 2010s and early 2020s this approach was increasingly applied to a new sector: DTC brands. Consumer traction and revenue growth were the key ingredients for strong valuations in both the private and public markets.

Crash

The reasons why investors have changed their minds about this are covered extensively elsewhere. While Crunchbase’s summary that “VCs No Longer Do DTC” is somewhat overstated, it captures the mood. Venture and growth investing in the DTC space has slowed dramatically, since the DTC model is no longer viewed in the same way: it isn’t a close proxy for the SaaS model after all. And with CPMs rising inexorably over time, DTC brands realised that compared to the middleman they had “cut out” (retail), the middlemen they had replaced it with (primarily Meta and Google) had become even more expensive.

All is not lost. Not all early-stage investors have abandoned DTC and it should be noted that much of the collapse in VC funding since 2021 is related to one specific phenomenon: the irrational exuberance around the Amazon “aggregator” sector. If these investments are removed from the analysis, the decline in DTC funding is far less precipitous.

However, the early-stage investors who are still investing in DTC brands are doing so at lower valuations. Their criteria are more stringent. They require more evidence of success and put even more emphasis on brand equity.

Private equity investors and acquirers have shifted their approach too. While there are still a few consumer private equity firms who will acquire a stand-out brand that is approaching breakeven, the vast majority require profitability before investment.

In this context, profitability has taken centre stage. Those DTC brands that can grow profitably are not only more investable, they don’t need the investment as much. In an environment where growth funding is far from certain, growing profitably (albeit more slowly) is a more reliable path.

Profitability and Valuation

So what impact does profitability really have on valuation? The public markets provide useful insight.

Public DTC brands have had a tumultuous few years. Rather than focusing on the frequently-discussed collapse in public DTC valuations in 2022, now that the dust has settled it is more relevant to look at how these brands are currently valued and the impact of profitability on these valuations. Hahnbeck’s proprietary CPG & DTC public market data is helpful in this regard.

If we take the 36 DTC brands listed on North American markets (full list below*), we can see that profitable companies do indeed achieve higher valuations. The average EV/Sales multiple for the 21 unprofitable companies in this cohort is 1.06x whereas the average for the 15 profitable companies is 1.84x.

Breaking down the profitable companies according to how profitable they are, we can see that the weighted average of those in the 0-10% net profit margin bracket traded at an average EV/Sales multiple 1.70x. The average was lifted by the one company in the 10-20% net profit bracket (Oddity Tech, with a market cap of $2.6Bn). On the other hand, Solo Brands, the only company in the dataset with net margins above 20%, bucked the trend, trading at a lower multiple of 0.72x, although with a market cap of only $120m this has less impact on the average.

* DTC brands included in this analysis:

a.k.a. Brands Holding Corp.

Allbirds Inc.

BARK Inc.

Beacn Wizardry and Magic Inc.

bebe Stores Inc.

Brilliant Earth Group Inc.

Bruush Oral Care Inc.

Connexa Sports Technologies Inc.

Cricut Inc.

DDC Enterprise Limited

Digital Brands Group Inc.

Duluth Holdings Inc.

FIGS Inc.

Goodfood Market Corp.

Grounded People Apparel Inc.

Hims & Hers Health Inc.

Kidpik Corp.

Kits Eyecare Ltd.

Lands' End Inc.

LSEB Creative Corp.

Lulu's Fashion Lounge Holdings Inc.

Mangoceuticals Inc.

Mene Inc.

MGO Global Inc.

Nature's Sunshine Products Inc.

Oddity Tech Ltd.

Peloton Interactive Inc.

Purple Innovation Inc.

Solo Brands Inc.

The Children's Place Inc.

The Lovesac Company

Torrid Holdings Inc.

TUT Fitness Group Inc.

Vegano Foods Inc.

Warby Parker Inc.

Willamette Valley Vineyards Inc.

Note that lists of publicly-traded DTC brands often include companies such as Lululemon, which reports that its “DTC” channel represents the majority of sales. However, in the case of Lululemon (as well as Canada Goose and a number of others), this definition of “DTC” includes not only website sales but sales via company-owned retail stores, drastically distorting the picture. Often the company-owned retail channel dramatically exceeds the true DTC website channel. We have excluded all of these firms from the above analysis.

The same trend is apparent in the CPG sector as a whole (a total of 474 companies traded on the North American markets). As would be expected in the broader CPG sector, where revenue has never really been taken as a proxy for profit, those companies with positive trailing net profits trade at higher valuations (1.93x sales) than those making net losses (0.69x). In fact, at every net margin bracket, companies with higher profitability are on average more valuable than less profitable ones.

This correlation may not mean causation, but the data is certainly interesting. Profitability is associated with a premium in both the broader CPG sector and in the specific DTC sector, although the premium is lower in the latter group.

Today vs 2021

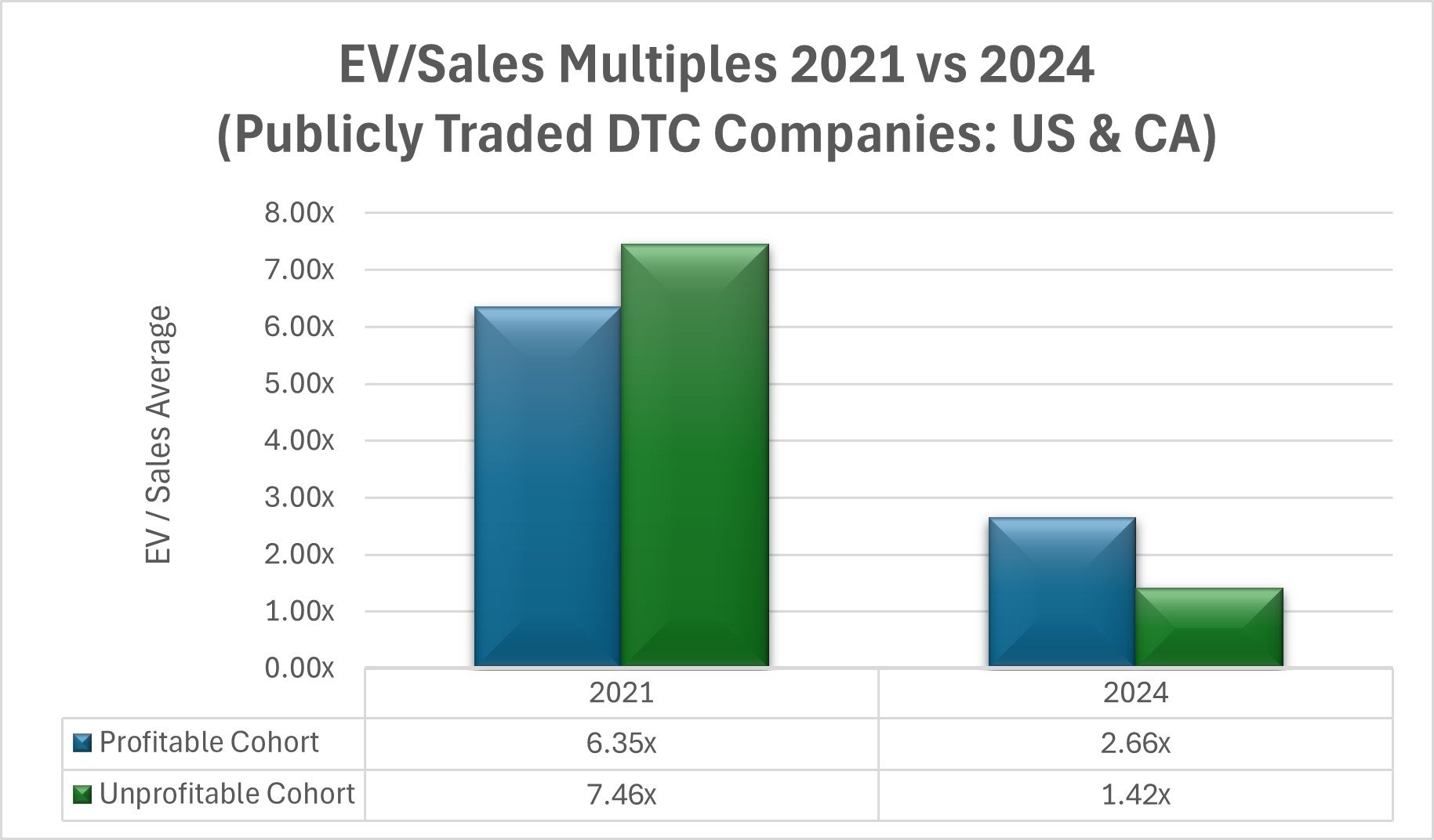

It’s interesting to note that in the case of DTC brands, this “profitability premium” was not always the case. In fact, the opposite was true.

Note that these cohorts are slightly different to those discussed above, since we have only included the 28 DTC companies that existed as publicly-traded entities on North American markets in both the 2021 and 2024 periods.

While the dramatic reduction in the valuation of the entire group of publicly-traded DTC brands is perhaps the most striking point on this table, it is not the focus of this article, since it has been discussed at length elsewhere. What is relevant to the current discussion is the fact that in 2021, unprofitable DTC brands (including the so-called “DTC Darlings”) were more valuable than profitable ones, on a weighted average basis. During the subsequent market shakeout in 2022, those brands with negative net margins saw their valuations decline even more rapidly than the DTC market as a whole and now achieve substantially lower valuation multiples than those with positive net margins.

Channel Mix and Valuation

The profitability analysis above includes only those companies whose largest channel is sales via the company’s own website. But a number of DTC brands derive a significant percentage of sales from retail, including several where company-owned stores are the largest channel. Adding these brands (Lululemon, YETI and the much smaller Laird Superfood) to the DTC cohort above, we can see the difference in valuation.

Perhaps unsurprisingly, adding more companies with a substantial retail channel to the cohort causes the weighted average valuation multiple to increase.

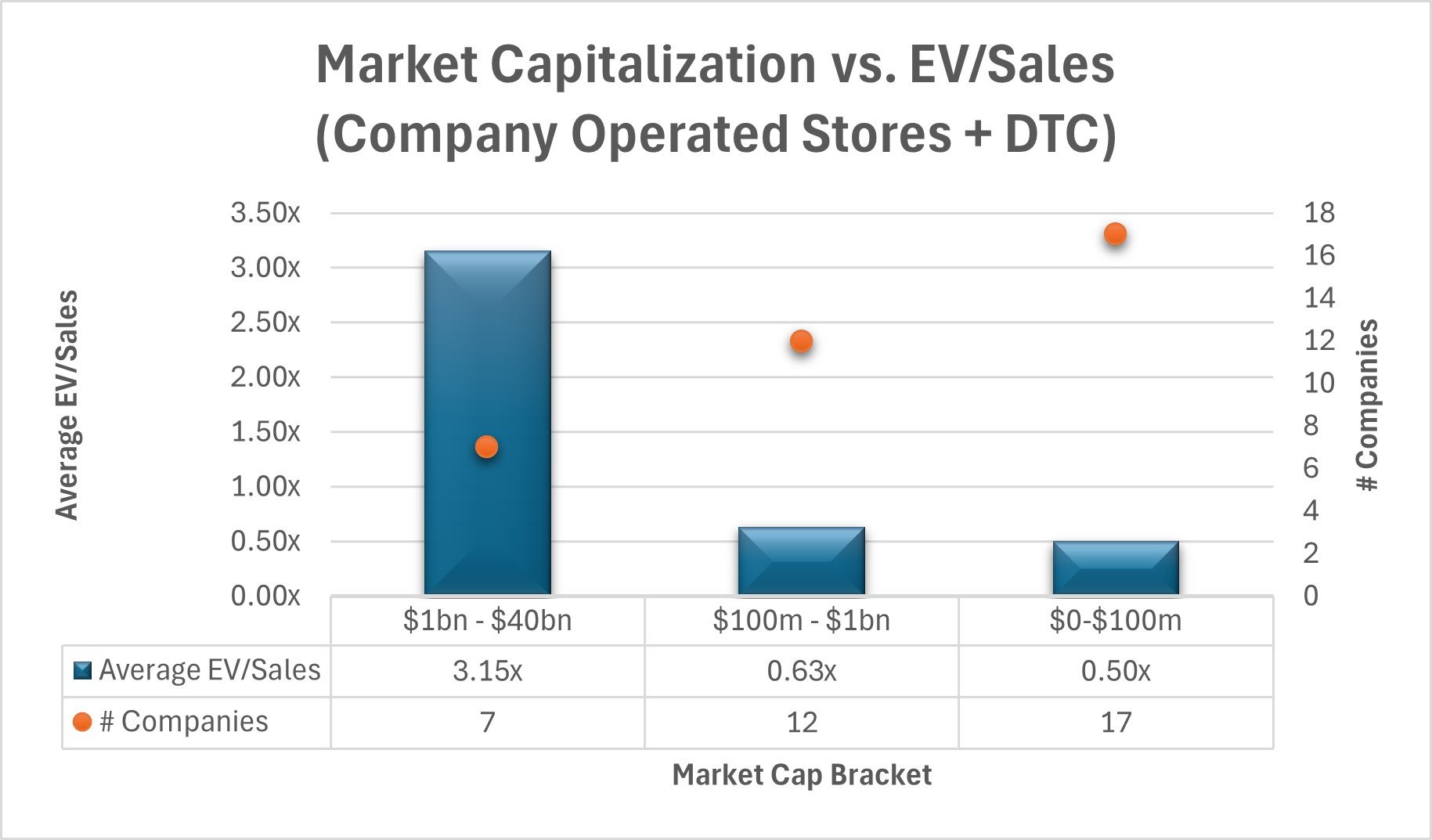

Size Matters

An important point not to overlook is the impact of scale. Larger businesses are valued at higher multiples. The largest DTC companies (those with a market cap of > $1Bn), are valued at substantially higher multiples than the ones below the $1Bn level.

Bringing Lululemon and YETI into the cohort not only added their retail store presence into the analysis, it also substantially increased the market cap of the group, contributing to the increase in valuation multiple.

However, this does not mean that the retail channel point is moot. The fact is that having a substantial retail presence is associated with larger size. E-commerce penetration is still only 15-16% in the United States, meaning that retail is approximately 85%. While most new brands are DTC-first, the fact remains that retail is where the scale is.

Privately-Held DTC Brands

For smaller, privately-held companies, this point certainly holds true. Early-stage investors and acquirers understand that early success in retail bodes well for the future, since the TAM in retail is simply much larger than the online equivalent. They attribute higher valuations as a result. In fact, almost all of the most successful founder-owned CPG brand exits (>$100m) of the past few years were brands that had a significant retail presence, even if they were DTC-first. We expect this trend to continue.

Athleisure brand Vuori exemplifies these points. With its most recent funding round valuing the company at $5.5Bn, it is the largest privately-held CPG brand, but it differs from the DTC Darlings of 2021 in a number of ways. Firstly, the company struggled to raise capital in the first few years of its existence, forcing it to focus on profitability. Without being able to pump VC dollars into advertising to feed the DTC flywheel, Vuori scaled more slowly, but more sustainably. With profitable customer acquisition metrics and growing brand awareness through early success in retail (via wholesale partnerships with retailers such as REI), by 2019 the company was in the enviable position of not needing growth capital. When it finally raised a large $400m round from Softbank in 2021, the money was used to scale up an already profitable business (and reward early shareholders), whereas its DTC Darling peers were desperately growing their top line and working to convince markets that breakeven would be reached eventually. Today Vuori continues to focus on sustainable, profitable growth across both DTC and retail, including in its own retail stores.

Few brand owners have ambitions to reach the size of Vuori or Lululemon. But for those looking to achieve a $10m to $150m exit, there are a number of lessons from both the public and private markets about the ingredients for success.

Focusing on profitability is not only desirable, it is all but essential. Size matters, but using unprofitable customer acquisition to achieve scale no longer makes sense (unless the business is several years away from an exit or funding round). Utilising retail partnerships can be a highly effective way to accelerate growth and increase brand awareness while maintaining profitability. Since the retail channel is so much larger than e-commerce, early success in retail for DTC brands demonstrates to investors and acquirers that there is substantially more upside in future. The combination of these factors results in the highest valuations (and the greatest exit potential) in the DTC space.

Hahnbeck is a leading global M&A firm specialising in DTC & retail, with a focus on the $2m to $15m EBITDA range. If this sounds like your business and you would like to discuss M&A strategy, you can contact us at info@hahnbeck.com.